fjrigjwwe9r3SDArtiMast:ArtiCont

fiogf49gjkf0d

Calculate your tax liability before investing. Also, tax saving should be incidental and not the primary objective for investing in a particular product

The idea of saving more taxes sounds attractive to everyone, but few plan for it. Usually, most people look for investment avenues that provide tax benefit in the last 3 months of the financial year. Keeping tax saving as the primary objective, people often end up investing in the products that are not suitable for them.

“People have the old habit of deferring decisions till they hear the direct warning bell—of losing the opportunity to save taxes. Employees have to submit proofs of investments in December or January and this leads to a rush for tax saving investments,” said Sudhir Kaushik, co-founder and chief financial officer, TaxSpanner.com. But as we write every year, this year too, we want to state that before you choose to invest in a financial instrument, look at what it offers. Income tax savings should be incidental and not the primary objective behind choosing a particular product for investments. Here is how you should plan your choices.

Evaluate scope of saving tax

Before you buy just about any financial product and invest an arbitrary amount in it, estimate your total taxable income for the year and scope of saving on taxes by way of investing in different products.

Don’t forget to deduct the exempted income from the gross total income while calculating taxable income. For instance, house rent allowance, leave travel allowance and medical reimbursement are exempt from tax to some extent. If your net income is above the tax-free limit—Rs2.50 lakh for individuals below 60 years, Rs3 lakh for senior citizens (above 60), and Rs5 lakh for very senior citizens (above 80 years)—you could look for available deductions and avenues to save taxes (see table) .

Look at what you have

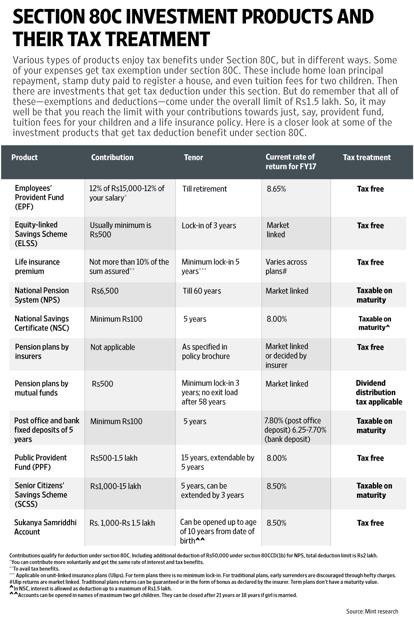

To know how much you can invest in each section, first look at your existing commitments that you have paid or need to pay this year. Check how much you have contributed towards the Employees’ Provident Fund (EPF), which directly gets deducted from your salary. Apart from life and health insurance premium, also consider the mandatory contributions towards Public Provident Fund, National Pension System (NPS) or Sukanya Samriddhi account. If you have invested in these, a minimum contribution is required every year. Most of these instruments provide deduction under section 80C of the income tax Act, which has an overall limit of Rs1.50 lakh. Remember, there is an additional tax benefit of Rs50,000 under section 80CCD (1B) for investment in NPS.

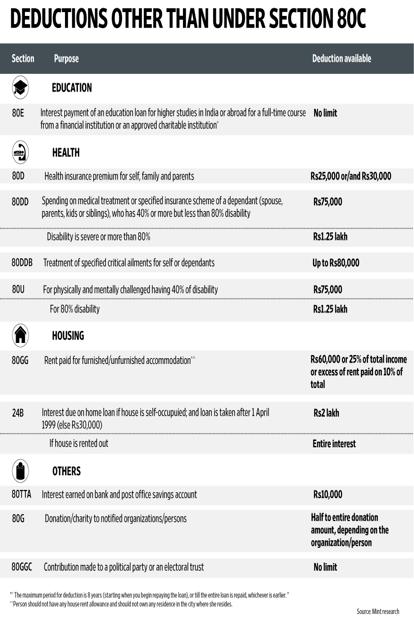

If you have exhausted the limit under section 80C through contributions to EPF, tuition fee and life insurance premiums, look for other deductions available to you. For instance, section 80D provides deduction against health insurance premium. Health insurance is a must-have product, and the premium qualifies for a deduction of up to Rs25,000. This limit includes the deduction of Rs5,000 allowed for preventive check-ups. For senior citizens, the limit is higher, at Rs30,000.

Evaluate various products

“Tax saving cannot be the be-all and end-all of investment decisions,” said Lovaii Navlakhi, founder and chief executive officer, International Money Matters Pvt. Ltd, a Bengaluru-based financial planning firm.

You should “choose the options available for balanced tax saving on the basis of your financial need, diversification and return on investment,” said Kaushik.

Besides that, “length of lock-in period, future liquidity needs and risk-reward of each instrument needs to be considered,” said Roopali Prabhu, head of investment products, Sanctum Wealth Management Pvt. Ltd. “The roots of each investment need to be in the asset allocation,” she added.

You should also evaluate the existing investments or contributions that you are making. “Nuances of instruments have been changing, for example: PPF rates are reviewed and aligned to the prevalent market levels more frequently,” said Prabhu.

It is not necessary that you need to continue investing in the product even if it is no longer suitable for you.

“Discard the sub-optimal investments. For example, high insurance premium policies without adequate risk cover should be converted into paid policies or surrendered, if the amount is exceeding the eligibility limit of section 80C,” said Kaushik.

While selecting a product, you also need to identify your goals and link them with investments. “Cash flow is an important factor to consider in this exercise: one cannot open a Public Provident Fund account if there is a fund requirement after 3 years. Even an ELSS (equity- linked savings scheme) may not be suitable for someone who needs the entire invested amount after exactly 3 years,” said Navlakhi. “Simply put, one needs to determine the goals, and then select the instruments,” he added.

Spend some time to evaluate your tax saving opportunities. Ideally, you should have done this at the beginning of the financial year, which would have given you time to plan in a better way. But if you have missed to do it this year, don’t forget to do it next time.